When it comes to investable themes, Mark Twain’s famous quote comes to mind: “History doesn’t always repeat itself, but it does rhyme.”

The quote is worth keeping in mind for investors who want a framework to contextualize the results of the U.S. election. After all, the parallels between the 2016 and 2024 electoral cycles are there—Donald Trump has won and the Republicans are now in control of both chambers of Congress. What’s more, Trump won this election with effectively the same platform (in broad strokes) that he did in 2016. Namely, an agenda centered on trade protectionism (notably against China and Mexico), tax cuts, de-regulation and anti-immigration policies.

Given that backdrop, it makes sense that investors are using the 2016 election as the departure point for what to expect going forward. In this note, our aim is to provide more clarity on what happened in markets in the early part of Trump’s term while also providing further context behind those developments and why the 2025 story could be different from 2017.

The Real Economy Back Then

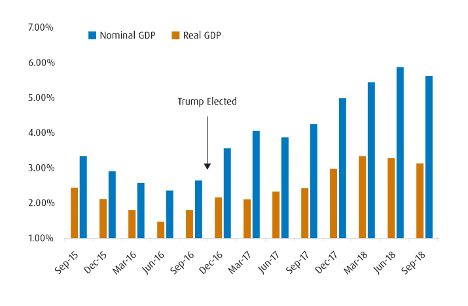

In 2017, Trump’s first year in office, the U.S. economy expanded by 5% nominally and 3% in real terms. Those are impressive numbers on their own, and if we delve a bit deeper, we see that was primarily due to healthy private sector spending. For instance, final sales to private domestic purchasers—which only looks at household and business spending—was up over 3% that year. That’s a healthy pace to be sure.

Chart 1 – Nominal and Real GDP Before and After Trump’s Win in 2016

Chart 1 – Nominal and Real GDP Before and After Trump’s Win in 2016

Source: U.S. Bureau of Economic Analysis (BEA).

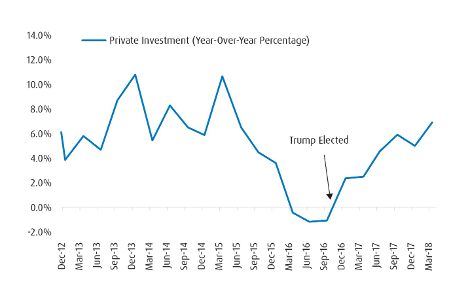

Put simply, the story of U.S. growth in 2017 was that of a massive wave of private sector spending. The most proximate reason for that was tax cuts. Recall, there was a high degree of anticipation for the Tax Cuts and Jobs Act, which included large corporate tax reductions (from 35% to 21%) and helped propel non-residential spending. When taken with Trump’s efforts to deregulate, it’s no wonder then sentiment indicators spiked aggressively that year.

Chart 2 – Increases in Private Investment Drove Growth After 2016 Election

Chart 2 – Increases in Private Investment Drove Growth After 2016 Election

Source: BEA.

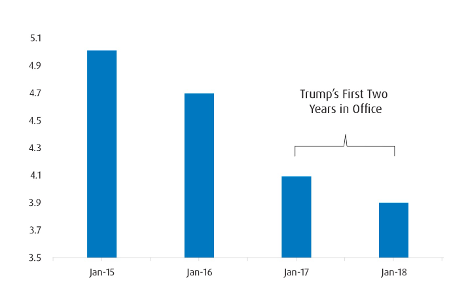

In the Labour sector, the unemployment rate fell by 0.6 percentage points (ppt) over the course of 2017 as the economy added over 2.1 million jobs. Inflation remained close to the U.S. Federal Reserve’s (Fed) 2% target for most of the year.

Chart 3 – Unemployment Rates at the Start of Each Year (%)

Chart 3 – Unemployment Rates at the Start of Each Year (%)

Source: U.S. Bureau of Labor Statistics (BLS)

When it comes to tariffs, things really kicked into higher gear in 2018. That year saw the imposition of Trump’s tariffs on solar panels, washing machines, and on steel/aluminum. That was also around the same time that the trade war between the U.S. and China escalated in a meaningful manner. The net result? The U.S. trade deficit went from US$479 billion at the end of 2016 to US$559 billion at the end of 2019. So, no—tariffs didn’t actually shrink the trade deficit as Trump thought they would.

Chart 4 – U.S. Goods and Services Trade Over Time (US$ Billions)

Chart 4 – U.S. Goods and Services Trade Over Time (US$ Billions)

Source: U.S. Census Bureau.

What Did the Markets Do Back Then?

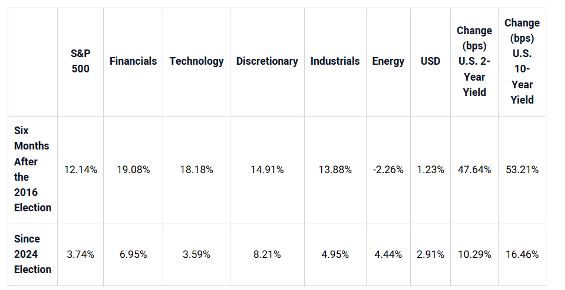

In the six months after the election date in 2016…

- The S&P 500 was up over 12%.

- Leading the way were Financials (+19%), Tech (+18%), Consumer Discretionary (+15%) and Industrials (+14%). Meanwhile, Energy lagged (-2.3%) over that period.

- Small caps were up 16.5%.

- S. 2-year yields rose by 32 basis points (bps) to 1.33%, while 10-year yields were up by 53 bps to 2.39%.

- The U.S. Dollar (USD) rose by just under 2% on a trade-weighted basis-with most of the gains against the Japanese Yen (JPY), Australian Dollar (AUD) and Mexican Peso (MXN). Gold prices declined by over 3%.

Fast forward to today, we see similar trends since the election (see Table 1). From a sectoral perspective, the notable exceptions are the Consumer Discretionary and Energy sectors, which are both outperforming relative to 2016. Additionally, the push higher in small caps thus far still looks quite modest relative to back then.

Table 1 – Comparing Market Moves Post 2016 and 2024 Elections

Source: BMO Global Asset Management, as of November 14, 2024.

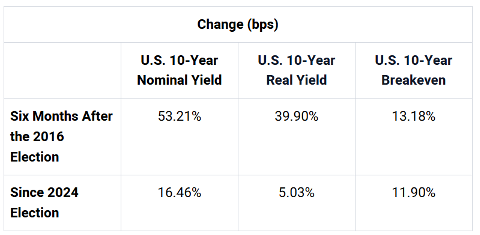

With respect to bonds and the rates market, it’s the move in U.S. 10-year yields that interests us. That’s primarily because the shift higher there was largely driven by moves in real yields1 (which were up by 40bps) as opposed to breakevens2 (up 13bps). The way to interpret this is that the market was of the view that Trump’s policies (most notably his tax cuts) were constructive for U.S. growth over the long term. To an extent, that’s the same narrative that the market is running with right now (see Table 2).

Table 2 – Comparing Shifts in U.S. 10-Year Yields

Source: BMO Global Asset Management, as of November 14, 2024.

For the USD, markets have moved much more quickly to reflect the impact of tariffs this time around. What’s also interesting now is that it’s the EUR that has underperformed the most among the majors. Meanwhile, the decline in gold prices now relative to 2016 implies there’s some degree of position overhang given the rally from earlier this year.

What Can We Conclude?

If we wanted to follow the 2016/17 playbook, we could just look at Table 1 above and see where the opportunities are. Assuming the same impulse holds into 2025, there’s a lot of juice left in Financials, Tech, small caps and Industrials. Additionally, there’s some more pain to be had in the rates space in the U.S.—as the delta in 2-year and 10-year yields is still well below what we saw in the first six months after the 2016 election.

However, we have some serious qualms about following the 2016/17 playbook to a tee this time around. Indeed, there are a few notable differences between where we were then and where we are now.

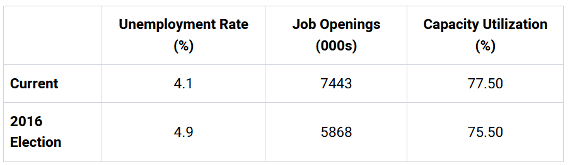

First, we’re now at a different point in the monetary policy cycle. In November 2016, the Fed was tightening policy slowly from a very stimulative level. Now, they’re easing from very restrictive levels to prevent a resurgence in price pressures. That’s largely because there’s less economic slack relative to 2016.

This last point is worth fleshing out. For the U.S. economy, 2017 was a year in which the stars aligned to allow for the sort of non-inflationary growth that is a central banker’s dream. But an important reason for that is the economy was operating with enough slack to provide that backdrop. For instance, the unemployment rate in November 2016 was still close to 5%—or well above the level we now would associate with generating inflationary pressures via the wage channel. That’s also backed up by where job openings and capacity utilization rates were at the time. In retrospect, there was plenty of room for Trump’s policies to generate growth without adding to inflation.

The same is not true today. The unemployment rate is above the cyclical lows, but still well below where we were in late-2016. At the very least that tells us that the proximity towards price pressures is closer relative to back then, which may force the Fed to keep policy at a more restrictive level. Long story short, we can’t count on the same Goldilocks-type of economic backdrop that we could for most of 2017.

Table 3 – There’s Less Economic Slack Now Relative to 2016

Source: BMO Global Asset Management, as of October 31, 2024.

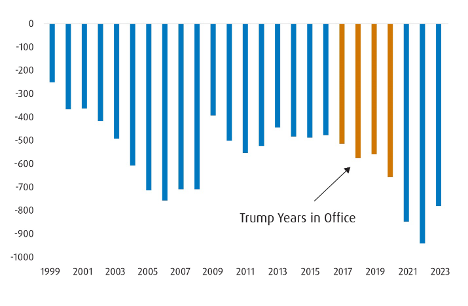

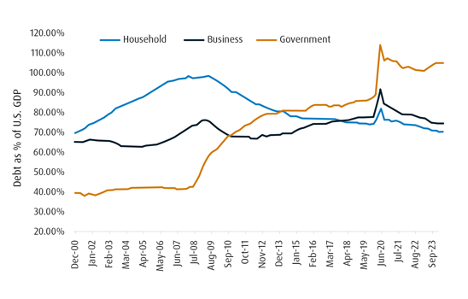

Second, the U.S. is already running large deficits. As a percentage of gross domestic product (GDP), the budget deficit was 3% when Trump took office in 2016 but is now closer to 6%. What’s more is that distribution of debt has become skewed, with more held by the government (as a percentage of GDP) relative to the private sector. This makes it much more important to spell out how deficits will be financed going forward – which could eventually impact legislation around tax cuts for the corporate sector.

Chart 5 – Distribution of Debt as a Percentage of GDP (%)

Source: Federal Reserve.

Both of the above points tell us that any uptick in growth driven by Trump’s policies is likely to be more inflationary now. Again, markets benefitted from non-inflationary growth in 2016, but the headroom for that isn’t quite as large this time around. That implies yields should remain elevated—as the Fed easing cycle is shallower and as inflation premiums rise further out the curve. By extension, that should work to ebb enthusiasm in sectors that are often sensitive to yields including Consumer Discretionary, Tech and Industrials.

Additionally, while it’s easy to see the USD rally continuing in the near-term, keep in mind that political themes (tariff increases most notably) tend to get discounted much more quickly into the FX market. True, there’s scant evidence that the impact of persistent/large budget deficits are being felt in the USD right now, but we could also look to the U.K. experience of late 2022 as an example of when markets can punish irresponsible fiscal policy. The implication here is that downward momentum in gold prices over the coming months (because of USD strength) is far from a lock.

Nevertheless, there are a few trends that we feel are reliable from here. For instance, large caps are a safe bet to continue performing, with Financials likely to continue in the pole position from a sectoral perspective. Indeed, Financials tend not to be as sensitive to gyrations in yields relative to other sectors – which gives us some degree of comfort with vehicles like BMO Equal Weight US Banks Index ETF (Ticker: ZBK).

Additionally, there’s reason to believe that the crypto rally can continue. Regular readers of ours will know that there’s a link between unconstrained deficit spending, central bank balance sheets and price action for Bitcoin. Nevertheless, we’d rather not go all in and would instead prefer funds that provide exposure to the crypto space while also allowing for some degree of diversification. From that lens, it makes sense to look at the BMO Ark Innovation Fund ETF (Ticker: ARKK).

When it comes to broader exposure, we’re still comfortable rolling with the BMO MSCI USA High Quality Index ETF (Ticker: ZUQ). From a factor perspective, quality outperformed in the first six months after the 2016 election, and we see little reason to suspect that won’t be the case this time around as well. Additionally, our U.S. focused long-short strategy ETF, the BMO Long Short US Equity ETF (Ticker) has performed relatively well since the election and we’ll be looking at adding some exposure there as well.

1 Real Yield: The rate of return an investor receives on an investment, taking into account the effect of inflation on the investment’s purchasing power.

2 Breakevens: The difference in yield between two interest-bearing securities, typically bonds, with the same maturity and credit risk. It’s a percentage-point spread that can be used to estimate inflation trends and determine the minimum rate of return needed to maintain wealth.

Disclaimer:

This communication is intended for information purposes only.

The ETF referred to herein is not sponsored, endorsed, or promoted by MSCI and MSCI bears no liability with respect to the ETF or any index on which such ETF is based. The ETF’s prospectus contains a more detailed description of the limited relationship MSCI has with the Manager and any related ETF.

The information contained herein is not, and should not be construed as, investment advice to any party. Investments should be evaluated relative to the individual’s investment objectives and professional advice should be obtained with respect to any circumstance.

BMO Global Asset Management is a brand name that comprises BMO Asset Management Inc., BMO Investments Inc., BMO Asset Management Inc. and BMO’s specialized investment management firms. BMO Mutual Funds are offered by BMO Investments Inc., a financial services firm and separate legal entity from the Bank of Montreal.

Commissions, management fees and expenses all may be associated with investments in exchange traded funds. Please read the ETF Facts or prospectus of the BMO ETFs before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all dividends or distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Exchange traded funds are not guaranteed, their values change frequently and past performance may not be repeated.

For a summary of the risks of an investment in the BMO ETFs, please see the specific risks set out in the BMO ETF’s prospectus. BMO ETFs trade like stocks, fluctuate in market value and may trade at a discount to their net asset value, which may increase the risk of loss. Distributions are not guaranteed and are subject to change and/or elimination.

BMO ETFs are managed by BMO Asset Management Inc., which is an investment fund manager and a portfolio manager, and a separate legal entity from Bank of Montreal.

Any statement that necessarily depends on future events may be a forward-looking statement. Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions. Although such statements are based on assumptions that are believed to be reasonable, there can be no assurance that actual results will not differ materially from expectations. Investors are cautioned not to rely unduly on any forward-looking statements. In connection with any forward-looking statements, investors should carefully consider the areas of risk described in the most recent prospectus.

The viewpoints expressed by the author represents their assessment of the markets at the time of publication. Those views are subject to change without notice at any time. The information provided herein does not constitute a solicitation of an offer to buy, or an offer to sell securities nor should the information be relied upon as investment advice. Past performance is no guarantee of future results. This communication is intended for informational purposes only.

“BMO (M-bar roundel symbol)” is a registered trademark of Bank of Montreal, used under licence.

")

{kind=link}